Stablecoin Volume Is Projected to Hit $719 Trillion by 2035: What Is Driving It

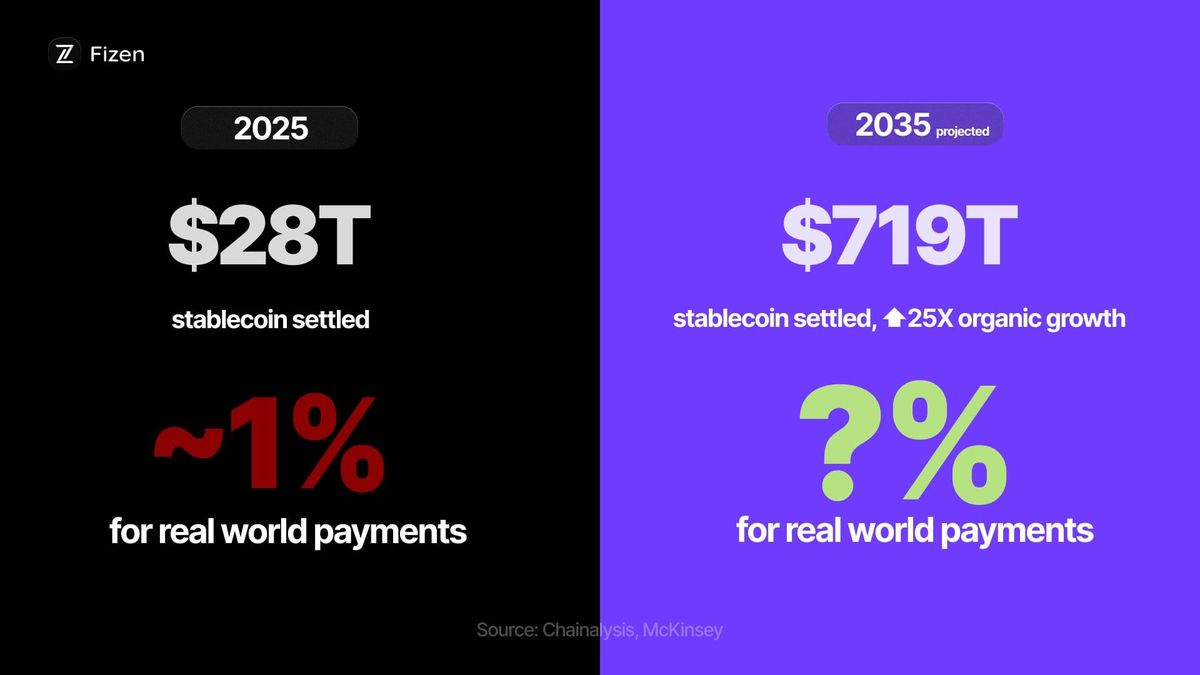

Chainalysis projects stablecoin adjusted volume could grow from $28 trillion (2025) to $719 trillion by 2035 on organic growth alone, or $1.5 quadrillion with generational wealth transfer and merchant POS adoption. McKinsey data shows less than 1% of current volume is real-world payments.

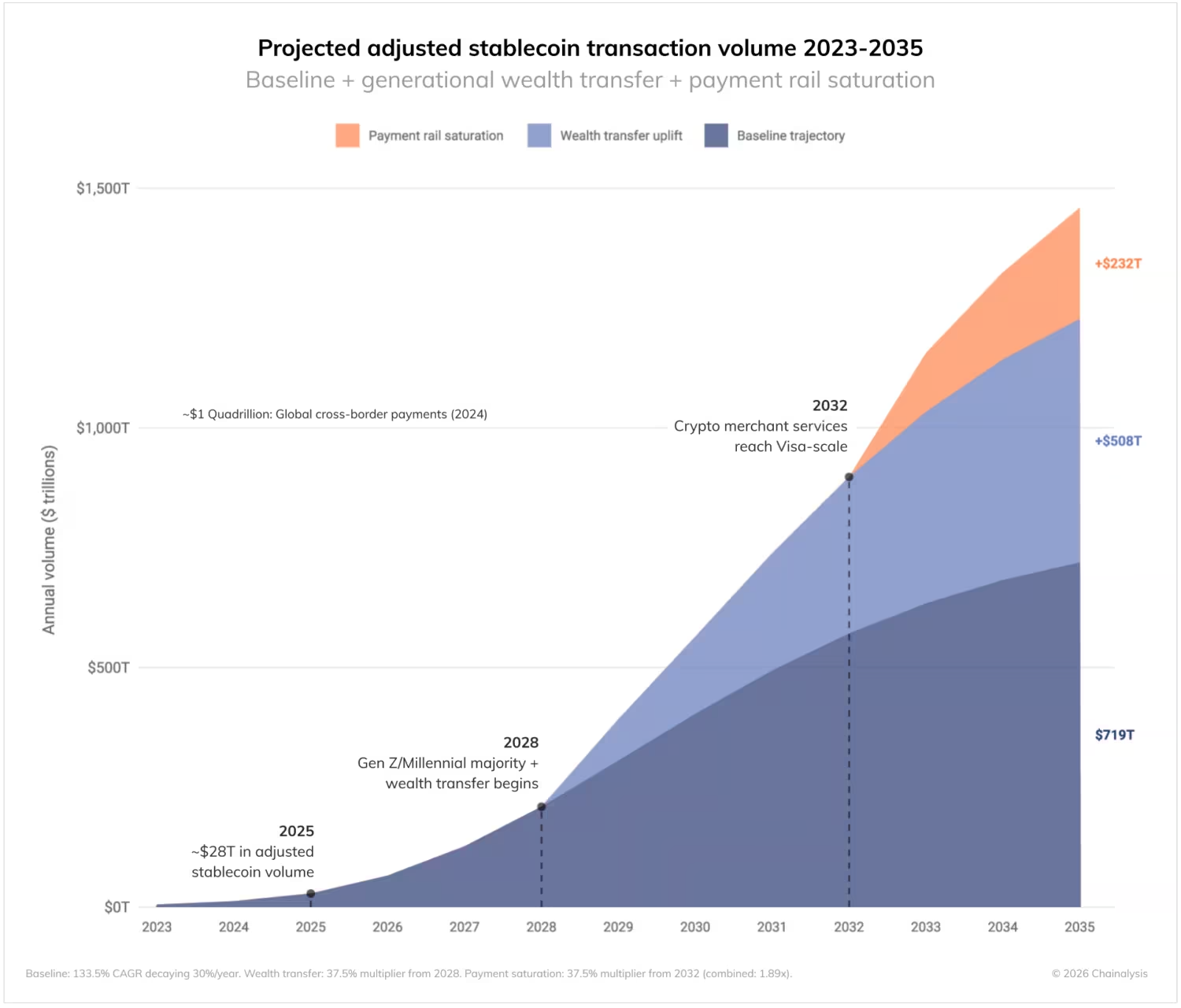

$719 trillion. That is the baseline projection for annual stablecoin transaction volume by 2035, according to Chainalysis (April 2026). With two macro accelerators factored in, the ceiling rises to $1.5 quadrillion, a figure that would exceed the entire global cross-border payments market.

For context: stablecoins processed $28 trillion in adjusted economic volume in 2025. The jump from $28 trillion to $719 trillion represents a 25x increase in a decade. The $1.5 quadrillion scenario is a 53x increase.

These are not speculative numbers. They are scenario models built on a growth rate that already exists.

The three engines behind the projection

Chainalysis breaks the forecast into three growth drivers, each with independent volume estimates:

1. Organic growth (baseline: $719 trillion)

Adjusted stablecoin volume, which filters out bot activity, MEV, and automated transactions to isolate genuine economic use, has been growing at a 133% compound annual growth rate since 2023. The $719 trillion baseline simply extends this existing trajectory forward with no new catalysts. No regulatory tailwinds, no merchant adoption wave. Just the current growth rate continuing.

2. Generational wealth transfer (+$508 trillion)

Between 2028 and 2048, an estimated $80, 100 trillion in wealth will move from Baby Boomers to Millennials and Gen Z. These are generations where nearly half already hold cryptocurrency, and 62% of Gen Z adults describe their crypto wallet as their primary savings vehicle.

Chainalysis estimates this shift alone could add $508 trillion in annual stablecoin volume by 2035, as inherited capital flows through crypto-native financial rails rather than traditional banking infrastructure.

3. Merchant point-of-sale adoption (+$232 trillion)

As stablecoin rails integrate with card networks and payment terminals, spending becomes as simple as swiping a card. This mirrors how credit cards replaced cash, slowly, then all at once.

Chainalysis estimates point-of-sale saturation across physical and e-commerce checkouts could add another $232 trillion in annual volume. Combined with the wealth transfer, this is what pushes the projection from $719 trillion to $1.5 quadrillion.

The gap between volume and real-world payments

Here is the tension in these numbers: stablecoins already moved $35 trillion in gross transfers in 2025. But according to a joint McKinsey and Artemis Analytics report (January 2026), less than 1% of that volume, roughly $390 billion, represented actual real-world payments: vendor invoices, remittances, payroll, consumer spending.

The rest was crypto trading, internal transfers, arbitrage, and protocol-level functions that never touched an end user.

Where the real payments are happening:

- B2B payments: $226 billion (up 733% YoY), cross-border vendor settlements and supply chain payments

- Remittances: $90 billion, global payroll and consumer-to-consumer transfers

- Capital markets: $80 billion, bond and securities settlement

Even with B2B growing at 733%, stablecoin payments represent just 0.01% of the $160 trillion global B2B market, and 0.02% of the $2 quadrillion+ total global payments volume.

For the Chainalysis projections to materialize, this share needs to grow by orders of magnitude.

What needs to happen for $719T to become real

The on-chain rails already work. Sending USDT from one wallet to another is instant and nearly free. The bottleneck is everything that happens after:

- Merchant acceptance: Most merchants cannot accept stablecoin payments at the point of sale. Card network integration is still early.

- Compliance infrastructure: The GENIUS Act (signed July 2025) created a U.S. federal framework. The OCC, FDIC, and Treasury have issued proposed rules. But regulation creates frameworks, it does not build payment rails.

- Fiat settlement: Converting a stablecoin transaction into a merchant’s local currency requires banking relationships, settlement layers, and liquidity, infrastructure that is still being built.

- Consumer UX: For most people, spending stablecoins is still harder than using a bank card. Closing this UX gap is what turns volume projections into actual adoption.

The Chainalysis and McKinsey data point to the same conclusion: the growth trajectory is real, the technology works, and the macro tailwinds are coming. The question is whether the infrastructure layer, the off-chain plumbing that connects on-chain balances to everyday commerce, can scale fast enough to capture it.

Stablecoin payment volumes are projected to match Visa and Mastercard combined between 2031 and 2039. The companies building that bridge are defining the next decade of payments infrastructure.

Sources

- Chainalysis, Stablecoin Utility and the Future of Payments, April 8, 2026

- McKinsey & Artemis Analytics, Stablecoins in Payments: What the Raw Transaction Numbers Miss, January 2026

- CoinDesk, Stablecoins moved $35 trillion, but only 1% for real-world payments, January 23, 2026

- U.S. OCC, GENIUS Act Notice of Proposed Rulemaking, February 25, 2026

Fizen Virtual Visa Card

The best card for SaaS, ChatGPT, Claude, Netflix, Spotify, Amazon, Google, Meta, Tiktok Ads. Spend USDT like cash globally.

This article is for informational purposes only and does not constitute financial or investment advice. Stablecoin projections cited are from third-party research and may not materialize. Fizen does not guarantee any returns or cashback amounts. Users should verify product availability in their jurisdiction. For more details, refer to Fizen Card Docs and Terms of Use.