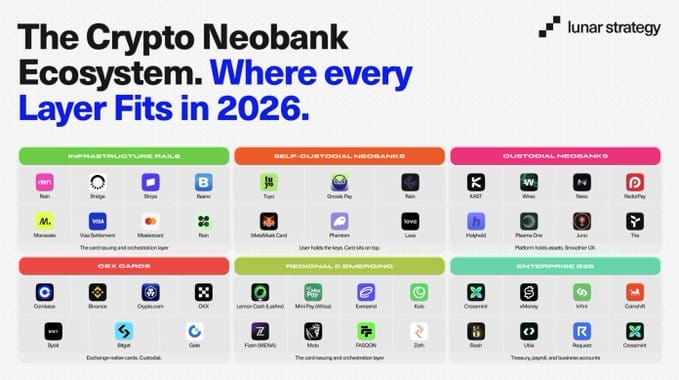

Fizen Just Landed on the 2026 Crypto Neobank Map

The 2026 neobank industry report is out, and Fizen is topped out in it. Here is the map, what it means, and why Fizen is built for APAC and MENA.

The 2026 crypto neobank landscape has been mapped, layer by layer, from the infrastructure giants to the regional challengers. Fizen is on that map.

That matters more than it sounds. The stablecoin market has passed $312 billion, up roughly 50% in a year. Stablecoin transfer volume overtook Visa and Mastercard combined, reaching $33 trillion in 2025. KAST raised at a $600 million valuation, Rain at $1.95 billion. The capital, the rails, and the users have all arrived. This is no longer a frontier experiment, it is infrastructure, and Fizen was named among the players building it.

Market data and the ecosystem map referenced here were compiled by Lunar Strategy (Jack Haldorsson). The Fizen analysis is our own.

The three models: who holds the keys

The category splits on one design choice, who controls the assets. Lunar Strategy's 2026 report groups the market into three models.

Self-custodial platforms keep funds in a wallet the user controls, with the card and account layer wrapped in a regulated structure. Tuyo, Gnosis Pay, and MetaMask Card sit here. Custodial neobanks hold assets for the user, which makes onboarding and yield delivery simpler but adds platform counterparty risk. KAST, Wirex, and Plasma One run this way. Incumbents adding crypto are led by Revolut, which reached 65 million users and processed $10.5 billion in stablecoin payments by the end of 2025 through a custodial product.

| Model | Who holds the keys | Examples | Tradeoff |

|---|---|---|---|

| Self-custodial | You | Tuyo, Gnosis Pay, MetaMask Card | Full control, more responsibility |

| Custodial | The platform | KAST, Wirex, Plasma One | Smoother UX, counterparty risk |

| Incumbent plus crypto | The platform | Revolut | Scale and trust, custodial |

What is driving adoption in 2026

Four forces, all measurable, explain why the category is scaling. The figures below come from Lunar Strategy's 2026 report and the sources it cites.

Remittances. The World Bank put the average cost to send $200 home at 6.36% in 2025, rising to 8.78% for Sub-Saharan Africa, with banks the most expensive channel at almost 15%. Stablecoin transfers settle in seconds for under 1%.

Inflation hedging. Stablecoin demand concentrates where local currencies are weakest. The report cites Chainalysis data showing Turkey at 4.3% of GDP, Argentina with more than 60% of crypto activity in dollar stablecoins, and Nigeria processing around $22 billion.

Yield. Many crypto neobanks have advertised 5 to 11% on stablecoin balances through DeFi vaults, against roughly 0.5% at a traditional bank. These returns are not bank interest and carry their own risk, which we cover below.

Payroll. A Pantera survey cited in the report found USDC and USDT make up over 90% of crypto salaries, as the share of workers paid in crypto tripled.

The infrastructure behind the boom

Launching a compliant card-and-account product used to take years. It now takes weeks. Rain, a Visa principal member, settles card transactions in stablecoins across multiple chains and 150+ countries, and raised $250 million at a $1.95 billion valuation in January 2026. Bridge, acquired by Stripe for $1.1 billion, handles stablecoin orchestration across 70+ countries, and Stripe's Open Issuance now lets businesses launch their own stablecoin. Visa and Mastercard both run stablecoin settlement programs. That commoditized stack is the real reason the number of crypto neobanks is accelerating.

Where regulation stands

The rules arrived in 2025. The US GENIUS Act, signed in July 2025, created the first federal stablecoin framework, with full reserves, monthly attestations, and a ban on issuers paying interest. The EU's MiCA enforces a similar yield ban and has delisted non-compliant stablecoins. The structural takeaway is simple: a stablecoin balance cannot pay deposit-style interest, so any yield runs through clearly disclosed third-party DeFi, which is not bank-insured. The friendliest jurisdictions for this infrastructure are the UAE, Singapore, Switzerland, and Hong Kong.

The risks worth knowing

The report is candid about the downside, and so are we. Almost every crypto neobank depends on a regulated partner bank, and if that relationship breaks, the card stops working. Token-funded models are fragile: Plasma's XPL fell roughly 94% from its late-2025 high, and price declines tend to undermine product credibility. Depeg risk is real, with one yield-bearing stablecoin briefly trading near $0.65 during the October 2025 market stress. And regulation, while improving, still shifts under the category's feet. Real interchange and spend revenue, not token price, is the more durable foundation.

Where Fizen sits on the 2026 map

Lunar Strategy sorted the 2026 crypto neobank ecosystem into six layers: infrastructure rails, self-custodial, custodial, exchange cards, regional and emerging, and enterprise B2B. Fizen sits in the regional and emerging layer, focused on APAC and MENA, the markets where stablecoin demand is highest.

Here is where Fizen lands:

Why APAC and MENA

The opportunity is concrete. The World Bank put the average cost to send $200 home at 6.36% in 2025, with banks the most expensive channel at nearly 15%. Stablecoins settle in seconds for a fraction of that. Across APAC and MENA, millions of people move money across borders every month, hedge against inflation, and already pay by QR. These are the conditions a stablecoin neobank is built for, and they are exactly where Fizen focuses.

Backed by Tether

In April 2025, Tether made a strategic investment in Fizen to strengthen global stablecoin utilization and self-custody solutions. Tether is the largest company in digital assets and the issuer of USDT, the most widely used stablecoin in the world. Its CEO, Paolo Ardoino, framed the investment around real-world payments and financial inclusion. You can read the announcement on Tether.io.

In a category where many products run on token price, that backing is a signal of substance.

An all-in-one app, not a single card

What separates a neobank from a card is breadth. Fizen runs as one app on one balance:

- Visa Card with FiPoint cashback up to 10%, issued through a MAS-licensed provider with DBS Bank Singapore.

- QR Pay across Southeast Asia: scan, pay USDT, and the merchant gets local fiat.

- Buy and sell crypto to fiat in-app, through P2P with Visa or bank transfer.

- In-app swap and bridge to move between assets and chains.

- eSIM for mobile data while you travel, paid with stablecoins.

- US stocks and gift cards, all from the same app.

Card, payments, crypto to cash, travel data, stocks, and gift cards, all from one login. That breadth is the difference between a neobank and a card with a wallet attached.

One app for card, QR payments, crypto to cash, travel data, stocks.

How Fizen rewards spending

Most cards make you accumulate points and hope they become a token someday. Fizen pays real value upfront. Every Fizen Card purchase earns FiPoint, up to 10% back, the moment you spend. Redeem it for a gift card every Happy Friday, or convert it to $FIZEN if you want the upside.

Real cashback now, optional upside later. Your call, not a gamble.

The category has crossed a threshold

Card-issuing infrastructure that once took years now takes weeks. The regulatory framework is arriving in parallel. The use cases driving adoption, remittances, inflation protection, and everyday spending, are real and growing across APAC and MENA. The names on the 2026 map are the ones positioned to define what comes next, and Fizen is one of them.

Your card. Your money. Your freedom.

Fizen Visa Card

The best card for SaaS, ChatGPT, Claude, Netflix, Spotify, Amazon, Google, Meta, Tiktok Ads. Spend USDT like cash globally.

FAQ

Is Fizen in the 2026 crypto neobank report?

What is a crypto-native neobank?

What region does Fizen serve?

Is Fizen really backed by Tether?

Is Fizen just a card?

Does Fizen pay interest or yield on stablecoins?

Source: market data and the ecosystem map referenced here were compiled by Lunar Strategy (Jack Haldorsson). See the original Crypto Neobank Ecosystem map on X: x.com/Jackhaldorsson. Figures are presented as reported by the source and are not independently verified by Fizen.

Nothing here is financial, investment, legal, or tax advice. FiPoint is a promotional reward, not cash, and its redemption value may vary. Cashback rates are not guaranteed and may change. Converting to $FIZEN is optional and never required. $FIZEN availability, allocation, and conversion ratios are determined by Fizen and may change at any time. Available to eligible users only, not to US Persons or residents of mainland China or Hong Kong.

Reward Program Terms · Schedule A · Promotion Master Terms · Card Terms · Master Terms of Use · Privacy Policy · Disclaimer