"Buy Now, Pay Maybe" Is Trending - But What If a Card Just Paid You Back Instead?

Tuyo's viral crypto card turns every purchase into a slot machine. There might be a smarter model — one where the math is on your side, not the algorithm's.

You've probably seen it on your timeline this week. A crypto debit card that sometimes doesn't charge you. "Buy now, pay maybe." Random free purchases. No odds disclosed. No transparency on when, or if, you'll ever get a free transaction.

Tuyo went viral. Fifty thousand users. Screenshots of free dinners and coffee runs flooding X. It's clever marketing. And it raises a real question that nobody's asking:

Why are we excited about maybe getting our money back, when cards could definitely pay you back?

Why "Buy Now, Pay Maybe" Went Viral (And Why That Matters)

The Tuyo card taps into something powerful: variable reward psychology. It's the same mechanic that makes slot machines addictive. You don't know when the reward is coming, so every swipe feels like a pull of the lever. Sometimes you win. Usually you don't.

Critics are already comparing it to gambling. And the comparison isn't unfair. No published odds. No disclosed frequency. An algorithm that "maximizes customer happiness", whatever that means.

But here's what the backlash misses: the desire behind the hype is completely valid. People want a card that feels generous. People want to feel like their spending isn't just money disappearing into a void. People want to get something back.

The question is whether "maybe" is really the best anyone can offer.

The Cashback Problem Nobody Talks About

Most debit cards with cashback give you 1-3% back. Some of the best cashback debit cards in 2026, Kast, Jupiter, Etherfi, top out around 1-5% on select categories with monthly caps.

Let's do the math. You spend $1,000 a month. Your card gives you 2% back. That's $20. Twenty dollars. For a thousand dollars of spending.

Meanwhile, the card issuer makes 1.5-3% in interchange fees on every transaction. They're earning more from your spending than you are. You're generating revenue for a bank and getting a fraction back as a thank-you.

The entire traditional cashback model is designed to make you feel rewarded while the house keeps most of the money. And now, with "buy now, pay maybe," the latest innovation is to make the reward random, so you can't even predict what you'll get.

Is this really the best we can do?

What If a Card Paid You More Than You Spent?

Here's the thought experiment that nobody in fintech seems to be having.

What if a crypto card existed where the cashback actually exceeded your transaction cost? Not 2%. Not the hope of a random freebie. What if you spent $5 on coffee and got $20 back, qualifying transaction, with published conditions?

Your first reaction is probably: "That's a Ponzi scheme."

Fair. Let's break it down.

The Ponzi version (how it usually fails): Company takes money from new users to pay "cashback" to old users. Works until growth stops. Then it collapses.

The treasury-backed version (how it could work): The company pre-funds a dedicated cashback reserve before any user spends a dime. Your card fee goes into a separate revenue pool. The two streams never touch. Cashback comes from the pre-funded treasury. Revenue comes from your fee plus interchange and FX margins.

In the second model, no user's cashback depends on another user's payment. The money is already sitting there before you swipe. And unlike "buy now, pay maybe," you know exactly how much you're getting and when.

The difference between these two models is the difference between a slot machine and a spreadsheet. One hopes you'll forget to do the math. The other invites you to.

Random vs. Deterministic: Which Card Model Actually Respects You?

This is the real debate the Tuyo hype should be sparking.

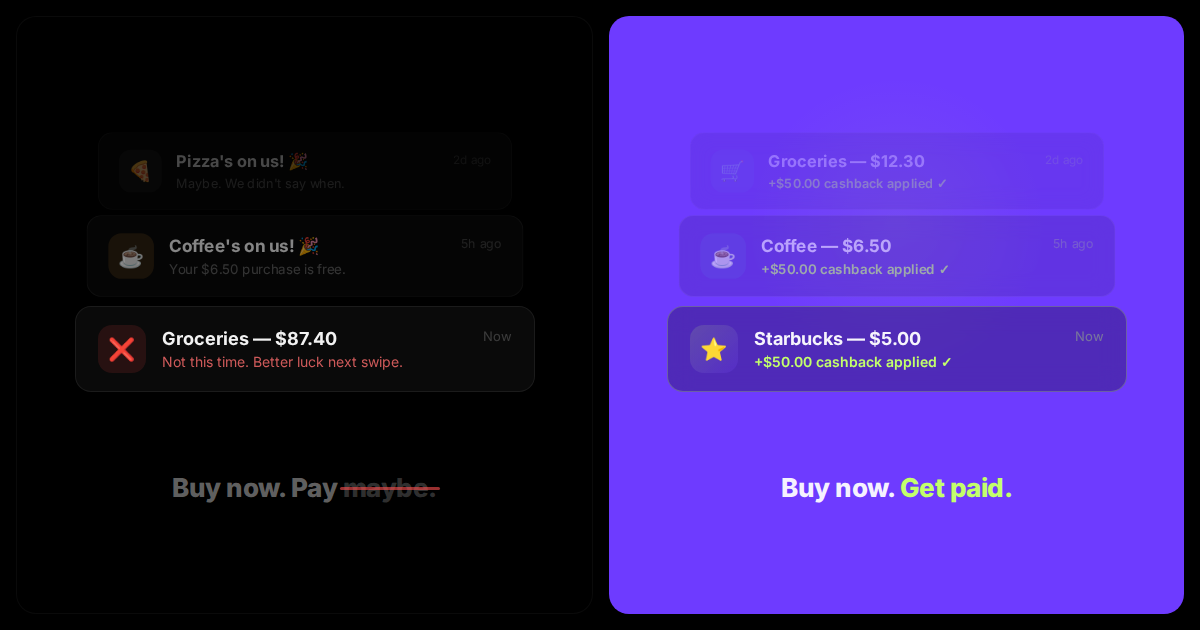

Random rewards (the Tuyo model): You have no idea if your next purchase will be free. The company controls the algorithm. No odds published. You might get 0% back forever. You might get lucky on a $5 coffee. You'll never get lucky on purpose.

Deterministic rewards (the alternative): You know upfront, $50 back per qualifying transaction, first 10 monthly transactions, for a 3-month qualifying period. You can calculate your total before you start. You can decide if the card fee is worth it. You can do math, not pray.

One model is designed to keep you swiping and hoping. The other is designed to keep you informed.

Both can be crypto cards. Both can use stablecoins. But the philosophy couldn't be more different.

"Too Good to Be True", Or Just Different?

We've been conditioned by crypto to distrust anything that sounds generous. And that instinct has saved a lot of people a lot of money.

But it also creates a blind spot. When something IS legitimately better, we dismiss it because we've been burned before.

Think about it. When Uber launched, people said "a stranger driving you around for less than a taxi? Scam." When Robinhood offered zero-commission trades, people said "how are they making money?" When cashback credit cards first appeared, people said "why would a bank pay me to spend?"

Every financial innovation sounds absurd until it doesn't.

The question isn't whether high cashback sounds too good to be true. The question is: what's the mechanism, and does the math check out?

How to Evaluate Any High-Cashback Crypto Card in 2026

If you're evaluating any card that promises more than the standard 1-3%, whether it's a "buy now, pay maybe" model or a flat high-cashback structure, here's your due diligence checklist:

Where does the cashback come from? If the answer is vague or hand-wavy ("our algorithm decides"), that's a marketing answer. A structural answer sounds like: "pre-funded treasury with transparent reserves, separate from card fee revenue."

Are the two money streams separated? Your card fee and your cashback should come from different pools. If they're mixed, you have Ponzi risk. If they're separated with auditable proof, you have a business model.

Is there a cap? Unlimited cashback doesn't exist. Any honest program tells you exactly how much you can earn, under what conditions, in what time window. A program that won't define its limits is hiding something.

Can you verify the reserves? A public dashboard showing treasury health isn't a nice-to-have. It's the minimum bar. If they can't show you the reserves backing your rewards, they don't have them.

Is quantity limited? Paradoxically, a card that's harder to get is more trustworthy. Limited issuance means the company has calculated how many users its treasury can support. Mass availability with outsized cashback = red flag.

Do you have to earn access? The most credible high-reward programs require qualification, KYC, community participation, referrals, a waiting list. If anyone can get in with no friction, the rewards are either tiny or unsustainable.

The Bottom Line

"Buy now, pay maybe" is fun. It's viral. It makes for great screenshots on X. But when the dopamine wears off and you check your actual cashback total after three months, you might find that "maybe" added up to almost nothing.

The alternative isn't boring. It's just honest. A card that tells you upfront: here's what you'll get, here's when, here's the conditions. No algorithm. No luck. No slot machine.

Spending money will never feel good. But knowing exactly what you'll get back? That changes the math.

The cards worth your attention don't gamify your money. They show you the spreadsheet and let you decide.

The ones worth paying attention to won't beg for your attention. They'll make you earn your way in.

Fizen Virtual Visa Card

The best card for SaaS, ChatGPT, Claude, Netflix, Spotify, Amazon, Google, Meta, Tiktok Ads. Spend USDT like cash globally.

See more in Guides & Comparisons

- Gift Cards vs Virtual Cards vs Crypto Cards, Which One Actually Works for Subscriptions?

- I Tried 4 Cards and None Worked, Why Banks Block International Online Payments

- The Hidden Fee Your Bank Charges Every Time You Pay in USD

- No Credit Card? Here's How People Actually Pay for Online Subscriptions

See more in AI Tools

- Perplexity Pro for Crypto Holders, USDT to Visa, No Off-Ramp

- GitHub Copilot + USDT, The Dev Card That Actually Works on Stripe

- USDT Visa Card for ChatGPT Plus, $20 Should Cost $20